The Retirement Wake-Up Call Older Millennials Can't Afford to Ignore

If you're a millennial in your 40s, the numbers may be more unsettling than you'd like to admit. According to a 2025 report by the Transamerica Center for Retirement Studies, the median retirement savings balance for older millennials sits at just $73,000. That figure is $427,000 short of the $500,000 many 40-somethings believe they'll need — and it's nowhere near the $1.6 million that financial experts actually recommend for a comfortable retirement.

With fewer than 20 years left before traditional retirement age, the margin for delay is razor-thin. But financial advisers are clear: it's not too late to turn things around. What it takes is honesty about where you stand, a concrete plan, and the willingness to make some uncomfortable decisions.

Why Older Millennials Are Falling So Far Behind

This isn't a story about financial irresponsibility. It's a story about timing. Older millennials — roughly those born between 1981 and 1988 — entered the workforce during or just after the Great Recession, one of the worst economic downturns in modern history. Many graduated with significant student loan debt into a job market that offered little stability and even less opportunity for wealth-building.

Just as this generation began to find its financial footing, new challenges arrived: skyrocketing housing costs, persistent inflation, rising interest rates, and stagnant wage growth. The result is a generation caught between the financial obligations of today and the retirement security they desperately need to build for tomorrow.

"Unfortunately, I see this shortfall often with my millennial clients. They came of age during the Great Recession and are now dealing with rising housing costs, inflation, and higher interest rates during some of their prime saving years. The focus is to make it through the month, not maximize retirement contributions," says Elias Friedman, founder and senior wealth adviser at Kadima Wealth in Schaumburg, IL.

That day-to-day financial pressure makes it incredibly difficult to think decades ahead. But those who don't begin acting now risk making an already difficult situation far worse.

The Role of Housing Costs in the Retirement Gap

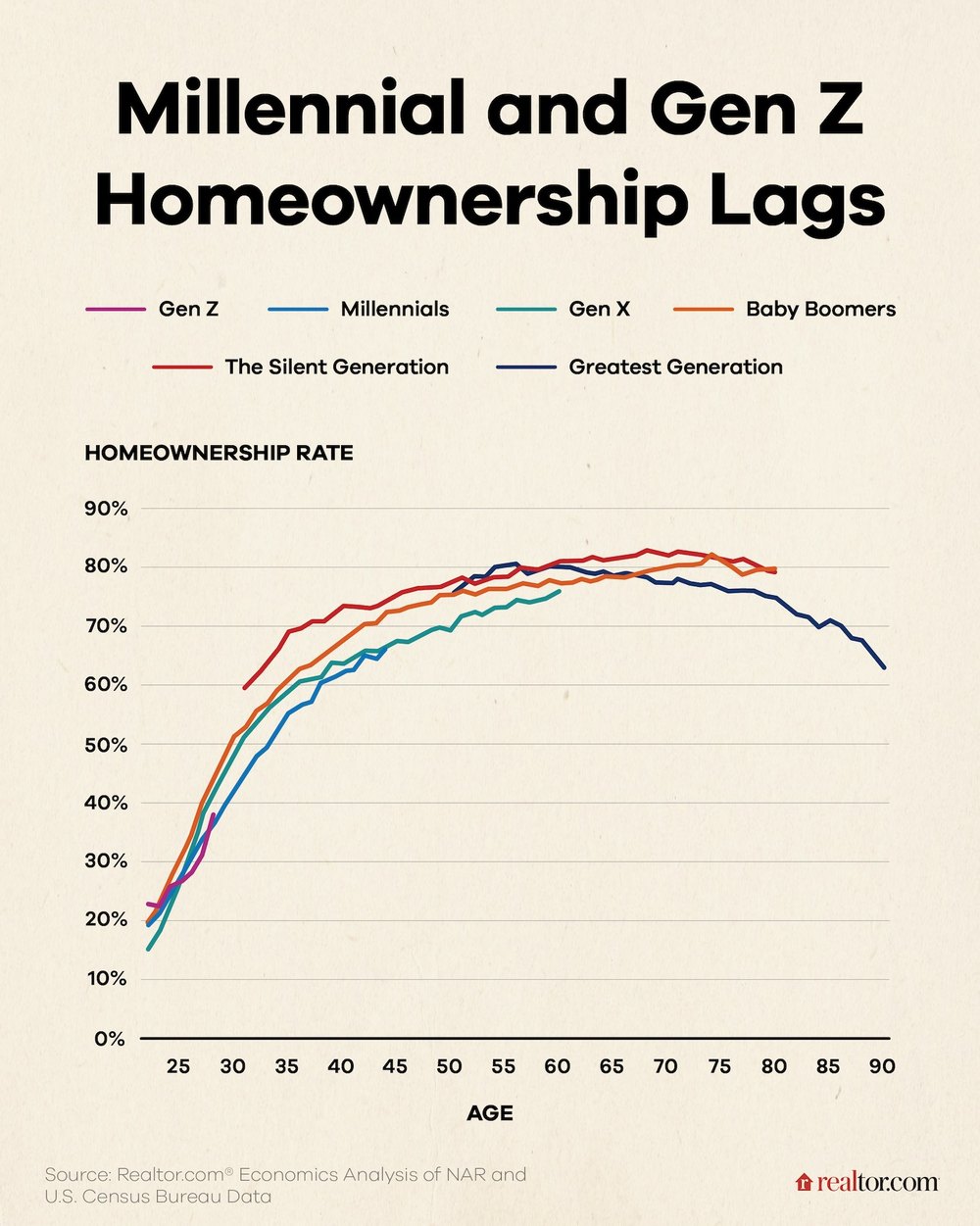

For previous generations, homeownership was the cornerstone of middle-class wealth. A modest home purchased in your 30s would appreciate steadily, giving you equity to draw on in retirement. For older millennials, that pathway has become far more complicated.

Mortgage payments and property taxes in many markets have risen faster than wages, leaving less discretionary income available for retirement contributions. Those who do own homes may find that a large percentage of their monthly income goes toward housing costs, leaving little room to max out 401(k) contributions or build a taxable investment account on the side.

For renters, the situation can be even more difficult. With rental prices climbing significantly over the past several years, many older millennials are spending a higher portion of their income on housing than any previous generation — all without building equity in the process.

How Much Do You Actually Need to Retire Comfortably?

The retirement savings targets that financial experts cite can feel staggering, but understanding them is the first step toward building a realistic plan. The commonly referenced figure of $1.6 million is based on the idea that you'll need roughly 80% of your pre-retirement income annually during retirement, and that your savings need to sustain you for 25 to 30 years.

Using the 4% rule — a widely accepted guideline suggesting you can withdraw 4% of your portfolio per year without running out of money — a $1.6 million nest egg would generate approximately $64,000 per year. Combined with Social Security benefits, that can provide a stable income for most retirees.

For older millennials currently sitting at $73,000 in savings, reaching $1.6 million in under 20 years is a serious challenge. But with aggressive contributions and smart investment strategies, narrowing the gap significantly is very achievable.

Practical Strategies to Close the Retirement Savings Gap

Maximize Tax-Advantaged Accounts First

The single most impactful thing you can do right now is contribute as much as possible to tax-advantaged retirement accounts. In 2025, the 401(k) contribution limit is $23,500, with an additional $7,500 catch-up contribution allowed for those aged 50 and over. If your employer offers matching contributions and you're not capturing the full match, you're leaving free money on the table. Individual Retirement Accounts (IRAs) offer another avenue, with contribution limits of $7,000 annually, or $8,000 if you're 50 or older.

Automate and Increase Contributions Gradually

If maxing out your 401(k) immediately isn't realistic, set up automatic contribution increases. Even bumping your contribution by 1% every six months creates meaningful compounding growth over time. Automating removes the temptation to spend money before it's invested and builds the habit of prioritizing your future self.

Reduce High-Interest Debt Strategically

Carrying high-interest debt while trying to invest is a losing battle. Credit card balances at 20% or more in interest can completely neutralize investment returns. Prioritizing debt payoff — particularly high-interest consumer debt — frees up cash flow that can then be redirected toward retirement savings.

Consider Delaying Retirement or Working Part-Time

For some older millennials, working a few extra years could make a dramatic difference. Delaying retirement from 65 to 67 not only gives your investments two more years to grow — it also increases your Social Security benefit, potentially by 8% per year after full retirement age. Part-time work in early retirement is another increasingly popular option that allows savings to remain invested longer.

Revisit Your Asset Allocation

With 15 to 20 years until retirement, older millennials still have time to hold a growth-oriented portfolio. If your investments are too conservative, you may be leaving significant growth on the table. Work with a financial adviser to ensure your allocation reflects both your timeline and your risk tolerance.

The Bottom Line: Act Now, Not Later

The retirement savings gap facing older millennials is real, and it's large. But it is not a reason for despair — it's a reason for action. The compounding power of time is still on your side, even if the window is narrowing. Every dollar you invest today has years to grow, and every financial habit you improve now compounds into a meaningfully better future.

The path forward requires facing the numbers honestly, building a plan that reflects your actual circumstances, and committing to small, consistent steps. As Elias Friedman and other advisers note, the focus for many millennials has understandably been surviving the present. The next chapter needs to also be about building the future — because the clock, quite simply, is ticking.